The Psychology of Money

Let me tell you the story of two investors, neither of whom knew each other, but whose paths crossed in an interesting way.

Grace Groner was orphaned at age 12. She never married. She never had kids. She never drove a car. She lived most of her life alone in a one-bedroom house and worked her whole career as a secretary. She was, by all accounts, a lovely lady. But she lived a humble and quiet life. That made the $7 million she left to charity after her death in 2010 at age 100 all the more confusing. People who knew her asked: Where did Grace get all that money?

But there was no secret. There was no inheritance. Grace took humble savings from a meager salary and enjoyed eighty years of hands-off compounding in the stock market. That was it.

Weeks after Grace died, an unrelated investing story hit the news.

Richard Fuscone, former vice chairman of Merrill Lynch’s Latin America division, declared personal bankruptcy, fighting off foreclosure on two homes, one of which was nearly 20,000 square feet and had a $66,000 a month mortgage. Fuscone was the opposite of Grace Groner; educated at Harvard and University of Chicago, he became so successful in the investment industry that he retired in his 40s to “pursue personal and charitable interests.” But heavy borrowing and illiquid investments did him in. The same year Grace Goner left a veritable fortune to charity, Richard stood before a bankruptcy judge and declared: “I have been devastated by the financial crisis … The only source of liquidity is whatever my wife is able to sell in terms of personal furnishings.”

The purpose of these stories is not to say you should be like Grace and avoid being like Richard. It’s to point out that there is no other field where these stories are even possible.

In what other field does someone with no education, no relevant experience, no resources, and no connections vastly outperform someone with the best education, the most relevant experiences, the best resources and the best connections? There will never be a story of a Grace Groner performing heart surgery better than a Harvard-trained cardiologist. Or building a faster chip than Apple’s engineers. Unthinkable.

But these stories happen in investing.

That’s because investing is not the study of finance. It’s the study of how people behave with money. And behavior is hard to teach, even to really smart people. You can’t sum up behavior with formulas to memorize or spreadsheet models to follow. Behavior is inborn, varies by person, is hard to measure, changes over time, and people are prone to deny its existence, especially when describing themselves.

Grace and Richard show that managing money isn’t necessarily about what you know; it’s how you behave. But that’s not how finance is typically taught or discussed. The finance industry talks too much about what to do, and not enough about what happens in your head when you try to do it.

This report describes 20 flaws, biases, and causes of bad behavior I’ve seen pop up often when people deal with money.

1. Earned success and deserved failure fallacy: A tendency to underestimate the role of luck and risk, and a failure to recognize that luck and risk are different sides of the same coin.

I like to ask people, “What do you want to know about investing that we can’t know?”

It’s not a practical question. So few people ask it. But it forces anyone you ask to think about what they intuitively think is true but don’t spend much time trying to answer because it’s futile.

Years ago I asked economist Robert Shiller the question. He answered, “The exact role of luck in successful outcomes.”

I love that, because no one thinks luck doesn’t play a role in financial success. But since it’s hard to quantify luck, and rude to suggest people’s success is owed to luck, the default stance is often to implicitly ignore luck as a factor. If I say, “There are a billion investors in the world. By sheer chance, would you expect 100 of them to become billionaires predominately off luck?” You would reply, “Of course.” But then if I ask you to name those investors – to their face – you will back down. That’s the problem.

The same goes for failure. Did failed businesses not try hard enough? Were bad investments not thought through well enough? Are wayward careers the product of laziness?

In some parts, yes. Of course. But how much? It’s so hard to know. And when it’s hard to know we default to the extremes of assuming failures are predominantly caused by mistakes. Which itself is a mistake.

People’s lives are a reflection of the experiences they’ve had and the people they’ve met, a lot of which are driven by luck, accident, and chance. The line between bold and reckless is thinner than people think, and you cannot believe in risk without believing in luck, because they are two sides of the same coin. They are both the simple idea that sometimes things happen that influence outcomes more than effort alone can achieve.

After my son was born I wrote him a letter:

Some people are born into families that encourage education; others are against it. Some are born into flourishing economies encouraging of entrepreneurship; others are born into war and destitution. I want you to be successful, and I want you to earn it. But realize that not all success is due to hard work, and not all poverty is due to laziness. Keep this in mind when judging people, including yourself.

2. Cost avoidance syndrome: A failure to identify the true costs of a situation, with too much emphasis on financial costs while ignoring the emotional price that must be paid to win a reward.

Say you want a new car. It costs $30,000. You have a few options: 1) Pay $30,000 for it. 2) Buy a used one for less than $30,000. 3) Or steal it.

In this case, 99% of people avoid the third option, because the consequences of stealing a car outweigh the upside. This is obvious.

But say you want to earn a 10% annual return over the next 50 years. Does this reward come free? Of course not. Why would the world give you something amazing for free? Like the car, there’s a price that has to be paid.

The price, in this case, is volatility and uncertainty. And like the car, you have a few options: You can pay it, accepting volatility and uncertainty. You can find an asset with less uncertainty and a lower payoff, the equivalent of a used car. Or you can attempt the equivalent of grand theft auto: Take the return while trying to avoid the volatility that comes along with it.

Many people in this case choose the third option. Like a car thief – though well-meaning and law-abiding – they form tricks and strategies to get the return without paying the price. Trades. Rotations. Hedges. Arbitrages. Leverage.

But the Money Gods do not look highly upon those who seek a reward without paying the price. Some car thieves will get away with it. Many more will be caught with their pants down. Same thing with money.

This is obvious with the car and less obvious with investing because the true cost of investing – or anything with money – is rarely the financial fee that is easy to see and measure. It’s the emotional and physical price demanded by markets that are pretty efficient. Monster Beverage stock rose 211,000% from 1995 to 2016. But it lost more than half its value on five separate occasions during that time. That is an enormous psychological price to pay. Buffett made $90 billion. But he did it by reading SEC filings 12 hours a day for 70 years, often at the expense of paying attention to his family. Here too, a hidden cost.

Every money reward has a price beyond the financial fee you can see and count. Accepting that is critical. Scott Adams once wrote: “One of the best pieces of advice I’ve ever heard goes something like this: If you want success, figure out the price, then pay it. It sounds trivial and obvious, but if you unpack the idea it has extraordinary power.” Wonderful money advice.

3. Rich man in the car paradox.

When you see someone driving a nice car, you rarely think, “Wow, the guy driving that car is cool.” Instead, you think, “Wow, if I had that car people would think I’m cool.” Subconscious or not, this is how people think.

The paradox of wealth is that people tend to want it to signal to others that they should be liked and admired. But in reality those other people bypass admiring you, not because they don’t think wealth is admirable, but because they use your wealth solely as a benchmark for their own desire to be liked and admired.

This stuff isn’t subtle. It is prevalent at every income and wealth level. There is a growing business of people renting private jets on the tarmac for 10 minutes to take a selfie inside the jet for Instagram. The people taking these selfies think they’re going to be loved without realizing that they probably don’t care about the person who actually owns the jet beyond the fact that they provided a jet to be photographed in.

The point isn’t to abandon the pursuit of wealth, of course. Or even fancy cars – I like both. It’s recognizing that people generally aspire to be respected by others, and humility, graciousness, intelligence, and empathy tend to generate more respect than fast cars.

4. A tendency to adjust to current circumstances in a way that makes forecasting your future desires and actions difficult, resulting in the inability to capture long-term compounding rewards that come from current decisions.

Every five-year-old boy wants to drive a tractor when they grow up. Then you grow up and realize that driving a tractor maybe isn’t the best career. So as a teenager you dream of being a lawyer. Then you realize that lawyers work so hard they rarely see their families. So then you become a stay-at-home parent. Then at age 70 you realize you should have saved more money for retirement.

Things change. And it’s hard to make long-term decisions when your view of what you’ll want in the future is so liable to shift.

This gets back to the first rule of compounding: Never interrupt it unnecessarily. But how do you not interrupt a money plan – careers, investments, spending, budgeting, whatever – when your life plans change? It’s hard. Part of the reason people like Grace Groner and Warren Buffett become so successful is because they kept doing the same thing for decades on end, letting compounding run wild. But many of us evolve so much over a lifetime that we don’t want to keep doing the same thing for decades on end. Or anything close to it. So rather than one 80-something-year lifespan, our money has perhaps four distinct 20-year blocks. Compounding doesn’t work as well in that situation.

There is no solution to this. But one thing I’ve learned that may help is coming back to balance and room for error. Too much devotion to one goal, one path, one outcome, is asking for regret when you’re so susceptible to change.

5. Anchored-to-your-own-history bias: Your personal experiences make up maybe 0.00000001% of what’s happened in the world but maybe 80% of how you think the world works.

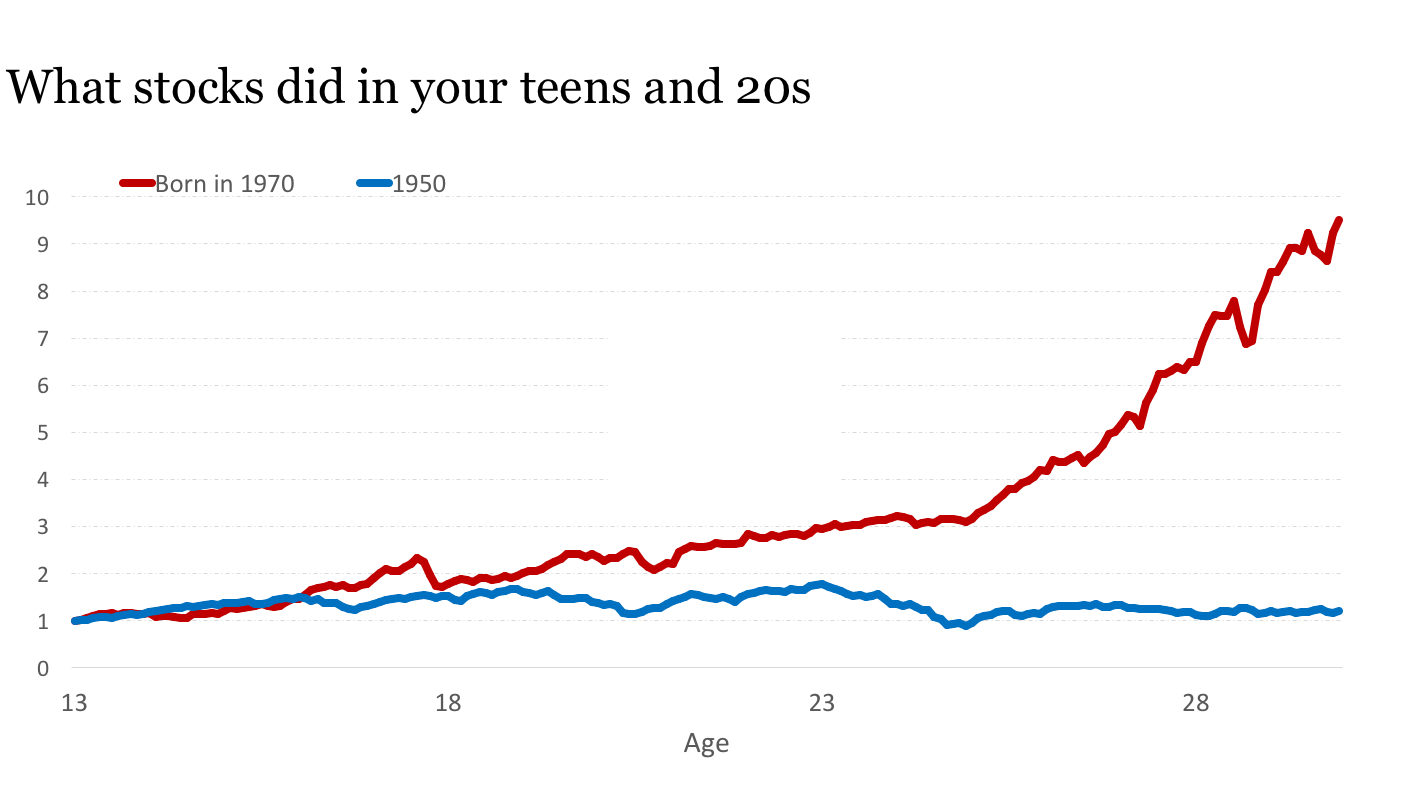

If you were born in 1970 the stock market went up 10-fold adjusted for inflation in your teens and 20s – your young impressionable years when you were learning baseline knowledge about how investing and the economy work. If you were born in 1950, the same market went exactly nowhere in your teens and 20s:

There are so many ways to cut this idea. Someone who grew up in Flint, Michigan got a very different view of the importance of manufacturing jobs than someone who grew up in Washington D.C. Coming of age during the Great Depression, or in war-ravaged 1940s Europe, set you on a path of beliefs, goals, and priorities that most people reading this, including myself, can’t fathom.

The Great Depression scared a generation for the rest of their lives. Most of them, at least. In 1959 John F. Kennedy was asked by a reporter what he remembered from the depression, and answered:

I have no first-hand knowledge of the depression. My family had one of the great fortunes of the world and it was worth more than ever then. We had bigger houses, more servants, we traveled more. About the only thing that I saw directly was when my father hired some extra gardeners just to give them a job so they could eat. I really did not learn about the depression until I read about it at Harvard.

Since no amount of studying or open-mindedness can genuinely recreate the power of fear and uncertainty, people go through life with totally different views on how the economy works, what it’s capable of doing, how much we should protect other people, and what should and shouldn’t be valued.

The problem is that everyone needs a clear explanation of how the world works to keep their sanity. It’s hard to be optimistic if you wake up in the morning and say, “I don’t know why most people think the way they do,” because people like the feeling of predictability and clean narratives. So they use the lessons of their own life experiences to create models of how they think the world should work – particularly for things like luck, risk, effort, and values.

And that’s a problem. When everyone has experienced a fraction of what’s out there but uses those experiences to explain everything they expect to happen, a lot of people eventually become disappointed, confused, or dumbfounded at others’ decisions.

A team of economists once crunched the data on a century’s worth of people’s investing habits and concluded: “Current [investment] beliefs depend on the realizations experienced in the past.”

Keep that quote in mind when debating people’s investing views. Or when you’re confused about their desire to hoard or blow money, their fear or greed in certain situations, or whenever else you can’t understand why people do what they do with money. Things will make more sense.

6. Historians are Prophets fallacy: Not seeing the irony that history is the study of surprises and changes while using it as a guide to the future. An overreliance on past data as a signal to future conditions in a field where innovation and change is the lifeblood of progress.

Geologists can look at a billion years of historical data and form models of how the earth behaves. So can meteorologists. And doctors – kidneys operate the same way in 2018 as they did in 1018.

The idea that the past offers concrete directions about the future is tantalizing. It promotes the idea that the path of the future is buried within the data. Historians – or anyone analyzing the past as a way to indicate the future – are some of the most important members of many fields.

I don’t think finance is one of them. At least not as much as we’d like to think.

The cornerstone of economics is that things change over time, because the invisible hand hates anything staying too good or too bad indefinitely. Bill Bonner once described how Mr. Market works: “He’s got a ‘Capitalism at Work’ T-shirt on and a sledgehammer in his hand.” Few things stay the same for very long, which makes historians something far less useful than prophets.

Consider a few big ones.

The 401(K) is 39 years old – barely old enough to run for president. The Roth IRA isn’t old enough to drink. So personal financial advice and analysis about how Americans save for retirement today is not directly comparable to what made sense just a generation ago. Things changed.

The venture capital industry barely existed 25 years ago. There are single funds today that are larger than the entire industry was a generation ago. Phil Knight wrote about his early days after starting Nike: “There was no such thing as venture capital. An aspiring young entrepreneur had very few places to turn, and those places were all guarded by risk-averse gatekeepers with zero imagination. In other words, bankers.” So our knowledge of backing entrepreneurs, investment cycles, and failure rates, is not something we have a deep base of history to learn from. Things changed.

Or take public markets. The S&P 500 did not include financial stocks until 1976; today, financials make up 16% of the index. Technology stocks were virtually nonexistent 50 years ago. Today, they’re more than a fifth of the index. Accounting rules have changed over time. So have disclosures, auditing, and market liquidity. Things changed.

The most important driver of anything tied to money is the stories people tell themselves and the preferences they have for goods and services. Those things don’t tend to sit still. They change with culture and generation. And they’ll keep changing.

The mental trick we play on ourselves here is an over-admiration of people who have been there, done that, when it comes to money. Experiencing specific events does not necessarily qualify you to know what will happen next. In fact it rarely does, because experience leads to more overconfidence than prophetic ability.

That doesn’t mean we should ignore history when thinking about money. But there’s an important nuance: The further back in history you look, the more general your takeaways should be. General things like people’s relationship to greed and fear, how they behave under stress, and how they respond to incentives tends to be stable in time. The history of money is useful for that kind of stuff. But specific trends, specific trades, specific sectors, and specific causal relationships are always a showcase of evolution in progress.

7. The seduction of pessimism in a world where optimism is the most reasonable stance.

Historian Deirdre McCloskey says, “For reasons I have never understood, people like to hear that the world is going to hell.”

This isn’t new. John Stuart Mill wrote in the 1840s: “I have observed that not the man who hopes when others despair, but the man who despairs when others hope, is admired by a large class of persons as a sage.”

Part of this is natural. We’ve evolved to treat threats as more urgent than opportunities. Buffett says, “In order to succeed, you must first survive.”

But pessimism about money takes a different level of allure. Say there’s going to be a recession and you will get retweeted. Say we’ll have a big recession and newspapers will call you. Say we’re nearing the next Great Depression and you’ll get on TV. But mention that good times are ahead, or markets have room to run, or that a company has huge potential, and a common reaction from commentators and spectators alike is that you are either a salesman or comically aloof of risks.

A few things are going on here.

One is that money is ubiquitous, so something bad happening tends to affect everyone, albeit in different ways. That isn’t true of, say, weather. A hurricane barreling down on Florida poses no direct risk to 92% of Americans. But a recession barreling down on the economy could impact every single person – including you, so pay attention. This goes for something as specific as the stock market: More than half of all households directly own stocks.

Another is that pessimism requires action – Move! Get out! Run! Sell! Hide! Optimism is mostly a call to stay the course and enjoy the ride. So it’s not nearly as urgent.

A third is that there is a lot of money to be made in the finance industry, which – despite regulations – has attracted armies of scammers, hucksters, and truth-benders promising the moon. A big enough bonus can convince even honest, law-abiding finance workers selling garbage products that they’re doing good for their customers. Enough people have been bamboozled by the finance industry that a sense of, “If it sounds too good to be true, it probably is” has enveloped even rational promotions of optimism.

Most promotions of optimism, by the way, are rational. Not all, of course. But we need to understand what optimism is. Real optimists don’t believe that everything will be great. That’s complacency. Optimism is a belief that the odds of a good outcome are in your favor over time, even when there will be setbacks along the way. The simple idea that most people wake up in the morning trying to make things a little better and more productive than wake up looking to cause trouble is the foundation of optimism. It’s not complicated. It’s not guaranteed, either. It’s just the most reasonable bet for most people. The late statistician Hans Rosling put it differently: “I am not an optimist. I am a very serious possibilist.”

8. Underappreciating the power of compounding, driven by the tendency to intuitively think about exponential growth in linear terms.

IBM made a 3.5 megabyte hard drive in the 1950s. By the 1960s things were moving into a few dozen megabytes. By the 1970s, IBM’s Winchester drive held 70 megabytes. Then drives got exponentially smaller in size with more storage. A typical PC in the early 1990s held 200-500 megabytes.

And then … wham. Things exploded.

1999 – Apple’s iMac comes with a 6 gigabyte hard drive.

2003 – 120 gigs on the Power Mac.

2006 – 250 gigs on the new iMac.

2011 – first 4 terabyte hard drive.

2017 – 60 terabyte hard drives.

Now put it together. From 1950 to 1990 we gained 296 megabytes. From 1990 through today we gained 60 million megabytes.

The punchline of compounding is never that it’s just big. It’s always – no matter how many times you study it – so big that you can barely wrap your head around it. In 2004 Bill Gates criticized the new Gmail, wondering why anyone would need a gig of storage. Author Steven Levy wrote, “Despite his currency with cutting-edge technologies, his mentality was anchored in the old paradigm of storage being a commodity that must be conserved.” You never get accustomed to how quickly things can grow.

I have heard many people say the first time they saw a compound interest table – or one of those stories about how much more you’d have for retirement if you began saving in your 20s vs. your 30s – changed their life. But it probably didn’t. What it likely did was surprise them, because the results intuitively didn’t seem right. Linear thinking is so much more intuitive than exponential thinking. Michael Batnick once explained it. If I ask you to calculate 8+8+8+8+8+8+8+8+8 in your head, you can do it in a few seconds (it’s 72). If I ask you to calculate 8x8x8x8x8x8x8x8x8, your head will explode (it’s 134,217,728).

The danger here is that when compounding isn’t intuitive, we often ignore its potential and focus on solving problems through other means. Not because we’re overthinking, but because we rarely stop to consider compounding potential.

There are over 2,000 books picking apart how Warren Buffett built his fortune. But none are called “This Guy Has Been Investing Consistently for Three-Quarters of a Century.” But we know that’s the key to the majority of his success; it’s just hard to wrap your head around that math because it’s not intuitive. There are books on economic cycles, trading strategies, and sector bets. But the most powerful and important book should be called “Shut Up And Wait.” It’s just one page with a long-term chart of economic growth. Physicist Albert Bartlett put it: “The greatest shortcoming of the human race is our inability to understand the exponential function.”

The counterintuitiveness of compounding is responsible for the majority of disappointing trades, bad strategies, and successful investing attempts. Good investing isn’t necessarily about earning the highest returns, because the highest returns tend to be one-off hits that kill your confidence when they end. It’s about earning pretty good returns that you can stick with for a long period of time. That’s when compounding runs wild.

9. Attachment to social proof in a field that demands contrarian thinking to achieve above-average results.

The Berkshire Hathaway annual meeting in Omaha attracts 40,000 people, all of whom consider themselves contrarians. People show up at 4 am to wait in line with thousands of other people to tell each other about their lifelong commitment to not following the crowd. Few see the irony.

Anything worthwhile with money has high stakes. High stakes entail risks of being wrong and losing money. Losing money is emotional. And the desire to avoid being wrong is best countered by surrounding yourself with people who agree with you. Social proof is powerful. Someone else agreeing with you is like evidence of being right that doesn’t have to prove itself with facts. Most people’s views have holes and gaps in them, if only subconsciously. Crowds and social proof help fill those gaps, reducing doubt that you could be wrong.

The problem with viewing crowds as evidence of accuracy when dealing with money is that opportunity is almost always inversely correlated with popularity. What really drives outsized returns over time is an increase in valuation multiples, and increasing valuation multiples relies on an investment getting more popular in the future – something that is always anchored by current popularity.

Here’s the thing: Most attempts at contrarianism is just irrational cynicism in disguise – and cynicism can be popular and draw crowds. Real contrarianism is when your views are so uncomfortable and belittled that they cause you to second guess whether they’re right. Very few people can do that. But of course that’s the case. Most people can’t be contrarian, by definition. Embrace with both hands that, statistically, you are one of those people.

10. An appeal to academia in a field that is governed not by clean rules but loose and unpredictable trends.

Harry Markowitz won the Nobel Prize in economics for creating formulas that tell you exactly how much of your portfolio should be in stocks vs. bonds depending on your ideal level of risk. A few years ago the Wall Street Journal asked him how, given his work, he invests his own money. He replied:

I visualized my grief if the stock market went way up and I wasn’t in it – or if it went way down and I was completely in it. My intention was to minimize my future regret. So I split my contributions 50/50 between bonds and equities.

There are many things in academic finance that are technically right but fail to describe how people actually act in the real world. Plenty of academic finance work is useful and has pushed the industry in the right direction. But its main purpose is often intellectual stimulation and to impress other academics. I don’t blame them for this or look down upon them for it. We should just recognize it for what it is.

One study I remember showed that young investors should use 2x leverage in the stock market, because – statistically – even if you get wiped out you’re still likely to earn superior returns over time, as long as you dust yourself off and keep investing after a wipeout. Which, in the real world, no one would actually do. They’d swear off investing for life. What works on a spreadsheet and what works at the kitchen table are ten miles apart.

The disconnect here is that academics typically desire very precise rules and formulas. But real-world people use it as a crutch to try to make sense of a messy and confusing world that, by its nature, eschews precision. Those are opposite things. You cannot explain randomness and emotion with precision and reason.

People are also attracted to the titles and degrees of academics because finance is not a credential-sanctioned field like, say, medicine is. So the appearance of a Ph.D stands out. And that creates an intense appeal to academia when making arguments and justifying beliefs – “According to this Harvard study …” or “As Nobel Prize winner so and so showed …” It carries so much weight when other people cite, “Some guy on CNBC from an eponymous firm with a tie and a smile.” A hard reality is that what often matters most in finance will never win a Nobel Prize: Humility and room for error.

11. The social utility of money coming at the direct expense of growing money; wealth is what you don’t see.

I used to park cars at a hotel. This was in the mid-2000s in Los Angeles, when real estate money flowed. I assumed that a customer driving a Ferrari was rich. Many were. But as I got to know some of these people, I realized they weren’t that successful. At least not nearly what I assumed. Many were mediocre successes who spent most of their money on a car.

If you see someone driving a $200,000 car, the only data point you have about their wealth is that they have $200,000 less than they did before they bought the car. Or they’re leasing the car, which truly offers no indication of wealth.

We tend to judge wealth by what we see. We can’t see people’s bank accounts or brokerage statements. So we rely on outward appearances to gauge financial success. Cars. Homes. Vacations. Instagram photos.

But this is America, and one of our cherished industries is helping people fake it until they make it.

Wealth, in fact, is what you don’t see. It’s the cars not purchased. The diamonds not bought. The renovations postponed, the clothes forgone and the first-class upgrade declined. It’s assets in the bank that haven’t yet been converted into the stuff you see.

But that’s not how we think about wealth, because you can’t contextualize what you can’t see.

Singer Rihanna nearly went broke after overspending and sued her financial advisor. The advisor responded: “Was it really necessary to tell her that if you spend money on things, you will end up with the things and not the money?”

You can laugh. But the truth is, yes, people need to be told that. When most people say they want to be a millionaire, what they really mean is “I want to spend a million dollars,” which is literally the opposite of being a millionaire. This is especially true for young people.

A key use of wealth is using it to control your time and providing you with options. Financial assets on a balance sheet offer that. But they come at the direct expense of showing people how much wealth you have with material stuff.

12. A tendency toward action in a field where the first rule of compounding is to never interrupt it unnecessarily.

If your sink breaks, you grab a wrench and fix it. If your arm breaks, you put it in a cast.

What do you do when your financial plan breaks?

The first question – and this goes for personal finance, business finance, and investing plans – is how do you know when it’s broken?

A broken sink is obvious. But a broken investment plan is open to interpretation. Maybe it’s just temporarily out of favor? Maybe you’re experiencing normal volatility? Maybe you had a bunch of one-off expenses this quarter but your savings rate is still adequate? It’s hard to know.

When it’s hard to distinguish broken from temporarily out of favor, the tendency is to default to the former, and spring into action. You start fiddling with the knobs to find a fix. This seems like the responsible thing to do, because when virtually everything else in your life is broken, the correct action is to fix it.

There are times when money plans need to be fixed. Oh, are there ever. But there is also no such thing as a long-term money plan that isn’t susceptible to volatility. Occasional upheaval is usually part of a standard plan.

When volatility is guaranteed and normal, but is often treated as something that needs to be fixed, people take actions that ultimately just interrupts the execution of a good plan. “Don’t do anything,” are the most powerful words in finance. But they are both hard for individuals to accept and hard for professionals to charge a fee for. So, we fiddle. Far too much.

13. Underestimating the need for room for error, not just financially but mentally and physically.

Ben Graham once said, “The purpose of the margin of safety is to render the forecast unnecessary.”

There is so much wisdom in this quote. But the most common response, even if subconsciously, is, “Thanks Ben. But I’m good at forecasting.”

People underestimate the need for room for error in almost everything they do that involves money. Two things cause this: One is the idea that your view of the future is right, driven by the uncomfortable feeling that comes from admitting the opposite. The second is that you’re therefore doing yourself economic harm by not taking actions that exploit your view of the future coming true.

But room for error is underappreciated and misunderstood. It’s often viewed as a conservative hedge, used by those who don’t want to take much risk or aren’t confident in their views. But when used appropriately it’s the opposite. Room for error lets you endure, and endurance lets you stick around long enough to let the odds of benefiting from a low-probability outcome fall in your favor. The biggest gains occur infrequently, either because they don’t happen often or because they take time to compound. So the person with enough room for error in part of their strategy to let them endure hardship in the other part of their strategy has an edge over the person who gets wiped out, game over, insert more tokens, when they’re wrong.

There are also multiple sides to room for error. Can you survive your assets declining by 30%? On a spreadsheet, maybe yes – in terms of actually paying your bills and staying cash-flow positive. But what about mentally? It is easy to underestimate what a 30% decline does to your psyche. Your confidence may become shot at the very moment opportunity is at its highest. You – or your spouse – may decide it’s time for a new plan, or new career. I know several investors who quit after losses because they were exhausted. Physically exhausted. Spreadsheets can model the historic frequency of big declines. But they cannot model the feeling of coming home, looking at your kids, and wondering if you’ve made a huge mistake that will impact their lives.

14. A tendency to be influenced by the actions of other people who are playing a different financial game than you are.

Cisco stock went up three-fold in 1999. Why? Probably not because people actually thought the company was worth $600 billion. Burton Malkiel once pointed out that Cisco’s implied growth rate at that valuation meant it would become larger than the entire U.S. economy within 20 years.

Its stock price was going up because short-term traders thought it would keep going up. And they were right, for a long time. That was the game they were playing – “this stock is trading for $60 and I think it’ll be worth $65 before tomorrow.”

But if you were a long-term investor in 1999, $60 was the only price available to buy. So you may have looked around and said to yourself, “Wow, maybe others know something I don’t.” And you went along with it. You even felt smart about it. But then the traders stopped playing their game, and you – and your game – was annihilated.

What you don’t realize is that the traders moving the marginal price are playing a totally different game than you are. And if you start taking cues from people playing a different game than you are, you are bound to be fooled and eventually become lost, since different games have different rules and different goals.

Few things matter more with money than understanding your own time horizon and not being persuaded by the actions and behaviors of people playing different games.

This goes beyond investing. How you save, how you spend, what your business strategy is, how you think about money, when you retire, and how you think about risk may all be influenced by the actions and behaviors of people who are playing different games than you are.

Personal finance is deeply personal, and one of the hardest parts is learning from others while realizing that their goals and actions might be miles removed from what’s relevant to your own life.

15. An attachment to financial entertainment due to the fact that money is emotional, and emotions are revved up by argument, extreme views, flashing lights, and threats to your wellbeing.

If the average American’s blood pressure went up by 3%, my guess is a few newspapers would cover it on page 16, nothing would change, and we’d move on. But if the stock market falls 3%, well, no need to guess how we might respond. This is from 2015: “President Barack Obama has been briefed on Monday’s choppy global market movement.”

Why does financial news of seemingly low importance overwhelm news that is objectively more important?

Because finance is entertaining in a way other things – orthodontics, gardening, marine biology – are not. Money has competition, rules, upsets, wins, losses, heroes, villains, teams, and fans that makes it tantalizingly close to a sporting event. But it’s even an addiction level up from that, because money is like a sporting event where you’re both the fan and the player, with outcomes affecting you both emotionally and directly.

Which is dangerous.

It helps, I’ve found, when making money decisions to constantly remind yourself that the purpose of investing is to maximize returns, not minimize boredom. Boring is perfectly fine. Boring is good. If you want to frame this as a strategy, remind yourself: opportunity lives where others aren’t, and others tend to stay away from what’s boring.

16. Optimism bias in risk-taking, or “Russian Roulette should statistically work” syndrome: An over attachment to favorable odds when the downside is unacceptable in any circumstance.

Nassim Taleb says, “You can be risk loving and yet completely averse to ruin.”

The idea is that you have to take risk to get ahead, but no risk that could wipe you out is ever worth taking. The odds are in your favor when playing Russian Roulette. But the downside is never worth the potential upside.

The odds of something can be in your favor – real estate prices go up most years, and most years you’ll get a paycheck every other week – but if something has 95% odds of being right, then 5% odds of being wrong means you will almost certainly experience the downside at some point in your life. And if the cost of the downside is ruin, the upside the other 95% of the time likely isn’t worth the risk, no matter how appealing it looks.

Leverage is the devil here. It pushes routine risks into something capable of producing ruin. The danger is that rational optimism most of the time masks the odds of ruin some of the time in a way that lets us systematically underestimate risk. Housing prices fell 30% last decade. A few companies defaulted on their debt. This is capitalism – it happens. But those with leverage had a double wipeout: Not only were they left broke, but being wiped out erased every opportunity to get back in the game at the very moment opportunity was ripe. A homeowner wiped out in 2009 had no chance of taking advantage of cheap mortgage rates in 2010. Lehman Brothers had no chance of investing in cheap debt in 2009.

My own money is barbelled. I take risks with one portion and am a terrified turtle with the other. This is not inconsistent, but the psychology of money would lead you to believe that it is. I just want to ensure I can remain standing long enough for my risks to pay off. Again, you have to survive to succeed.

A key point here is that few things in money are as valuable as options. The ability to do what you want, when you want, with who you want, and why you want, has infinite ROI.

17. A preference for skills in a field where skills don’t matter if they aren’t matched with the right behavior.

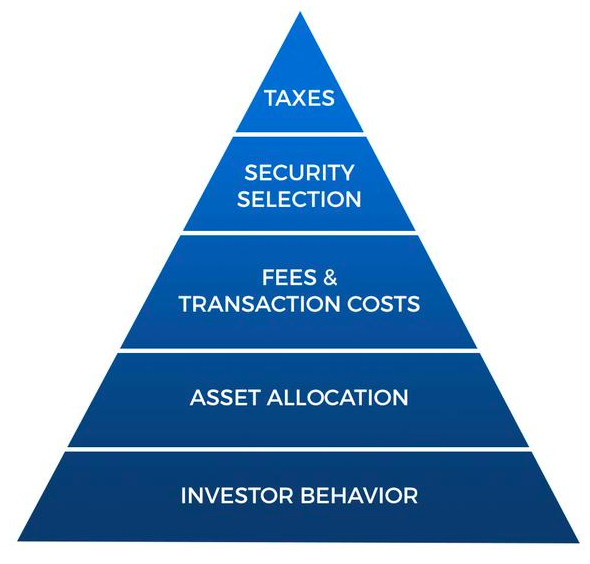

This is where Grace and Richard come back in. There is a hierarchy of investor needs, and each topic here has to be mastered before the one above it matters:

Richard was very skilled at the top of this pyramid, but he failed the bottom blocks, so none of it mattered. Grace mastered the bottom blocks so well that the top blocks were hardly necessary.

18. Denial of inconsistencies between how you think the world should work and how the world actually works, driven by a desire to form a clean narrative of cause and effect despite the inherent complexities of everything involving money.

Someone once described Donald Trump as “Unable to distinguish between what happened and what he thinks should have happened.” Politics aside, I think everyone does this.

There are three parts to this:

-

You see a lot of information in the world.

-

You can’t process all of it. So you have to filter.

-

You only filter in the information that meshes with the way you think the world should work.

Since everyone wants to explain what they see and how the world works with clean narratives, inconsistencies between what we think should happen and what actually happens are buried.

An example. Higher taxes should slow economic growth – that’s a common sense narrative. But the correlation between tax rates and growth rates is hard to spot. So, if you hold onto the narrative between taxes and growth, you say there must be something wrong with the data. And you may be right! But if you come across someone else pushing aside data to back up their narrative – say, arguing that hedge funds have to generate alpha, otherwise no one would invest in them – you spot what you consider a bias. There are a thousand other examples. Everyone just believes what they want to believe, even when the evidence shows something else. Stories over statistics.

{kind=link}

Accepting that everything involving money is driven by illogical emotions and has more moving parts than anyone can grasp is a good start to remembering that history is the study of things happening that people didn’t think would or could happen. This is especially true with money.

19. Political beliefs driving financial decisions, influenced by economics being a misbehaved cousin of politics.

I once attended a conference where a well known investor began his talk by saying, “You know when President Obama talks about clinging to guns and bibles? That is me, folks. And I’m going to tell you today about how his reckless policies are impacting the economy.”

I don’t care what your politics are, there is no possible way you can make rational investment decisions with that kind of thinking.

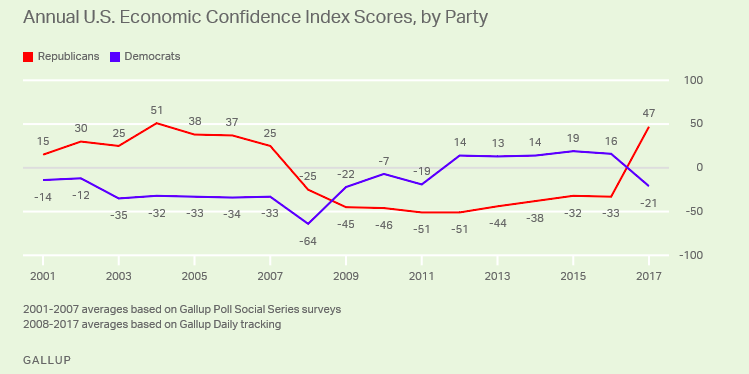

But it’s fairly common. Look at what happens in 2016 on this chart. The rate of GDP growth, jobs growth, stock market growth, interest rates – go down the list – did not materially change. Only the president did:

Years ago I published a bunch of economic performance numbers by president. And it drove people crazy, because the data often didn’t mesh with how they thought it should based on their political beliefs. Soon after a journalist asked me to comment on a story detailing how, statistically, Democrats preside over stronger economies than Republicans. I said you couldn’t make that argument because the sample size is way too small. But he pushed and pushed, and wrote a piece that made readers either cheer or sweat, depending on their beliefs.

The point is not that politics don’t influence the economy. But the reason this is such a sensitive topic is because the data often surprises the heck out of people, which itself is a reason to realize that the correlation between politics and economics isn’t as clear as you’d like to think it is.

20. The three-month bubble: Extrapolating the recent past into the near future, and then overestimating the extent to which whatever you anticipate will happen in the near future will impact your future.

News headlines in the month after 9/11 are interesting. Few entertain the idea that the attack was a one-off; the next massive terrorist attack was certain to be around the corner. “Another catastrophic terrorist attack is inevitable and only a matter of time,” one defense analyst said in 2002. “A top counterterrorism official says it’s ‘a question of when, not if,” wrote another headline. Beyond the anticipation that another attack was imminent was a belief that it would affect people the same way. The Today Show ran a segment pitching parachutes for office workers to keep under their desks in case they needed to jump out of a skyscraper.

Believing that what just happened will keep happening shows up constantly in psychology. We like patterns and have short memories. The added feeling that a repeat of what just happened will keep affecting you the same way is an offshoot. And when you’re dealing with money it can be a torment.

Every big financial win or loss is followed by mass expectations of more wins and losses. With it comes a level of obsession over the effects of those events repeating that can be wildly disconnected from your long-term goals. Example: The stock market falling 40% in 2008 was followed, uninterrupted for years, with forecasts of another impending plunge. Expecting what just happened to happen soon again is one thing, and an error in itself. But not realizing that your long-term investing goals could remain intact, unharmed, even if we have another big plunge, is the dangerous byproduct of recency bias. “Markets tend to recover over time and make new highs” was not a popular takeaway from the financial crisis; “Markets can crash and crashes suck,” was, despite the former being so much more practical than the latter.

Most of the time, something big happening doesn’t increase the odds of it happening again. It’s the opposite, as mean reversion is a merciless law of finance. But even when something does happen again, most of the time it doesn’t – or shouldn’t – impact your actions in the way you’re tempted to think, because most extrapolations are short term while most goals are long term. A stable strategy designed to endure change is almost always superior to one that attempts to guard against whatever just happened happening again.

If there’s a common denominator in these, it’s a preference for humility, adaptability, long time horizons, and skepticism of popularity around anything involving money. Which can be summed up as: Be prepared to roll with the punches.

Jiddu Krishnamurti spent years giving spiritual talks. He became more candid as he got older. In one famous talk, he asked the audience if they’d like to know his secret.

He whispered, “You see, I don’t mind what happens.”

That might be the best trick when dealing with the psychology of money.