Two Worlds: So Much Prosperity, So Much Skepticism

The demand for forecasts grows after a surprise. It’s quite an irony. Surprises make you feel like you’re not in control, which is when it feels best to grab the wheel with both hands, listening to those who tell you what happens next despite being blindsided by what just happened.

That’s where we are with Covid and the economy. Ten months after the surprise of our lifetimes, everyone wants a clear map of the future. Who wins? Who loses? When will travel recover? Will work be the same? Have we learned our lesson?

But the most important economic stories don’t require forecasts; they’ve already happened. And they tend to be the most overlooked, because when everyone’s focused on the future it’s easy to ignore what’s sitting right in front of us.

I want to tell you two of the biggest economic stories that aren’t getting enough attention.

One is that household finances might be in the best shape they’ve ever been in. Ever. That might sound crazy, and it’s easy to overlook because of the second story: Covid has dumped kerosene on wealth inequality in ways we’ve yet to fully grasp.

1. THE NEW BOOM

Near the peak of the Great Depression in 1931, an Ohio lawyer named Benjamin Roth wrote in his diary:

Magazines and newspapers are full of articles telling people to buy stocks, real estate etc. at present bargain prices. They say that times are sure to get better and that many big fortunes have been built this way. The trouble is that nobody has any money.

Nobody had any money. It was an exaggeration, but not much. The economy was broken, and – for years – people were in so much debt and had so little liquid resources that everything just stopped.

We’re now in our own generation’s Great Depression. But the situation could not be more different from what Roth felt 90 years ago.

Take three charts.

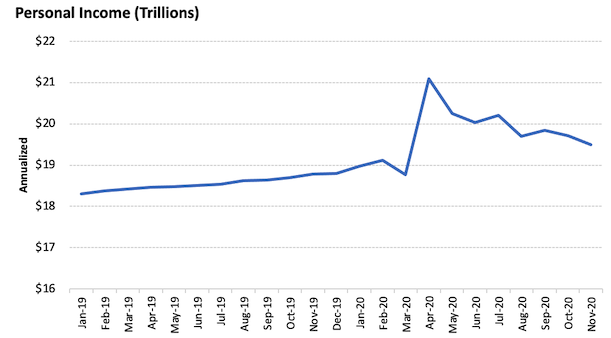

Here’s personal income:

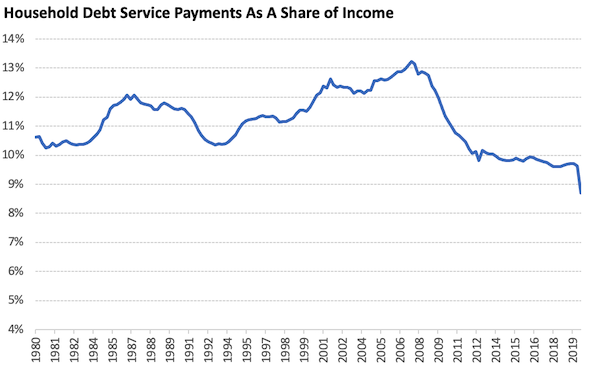

Here’s household debt payments:

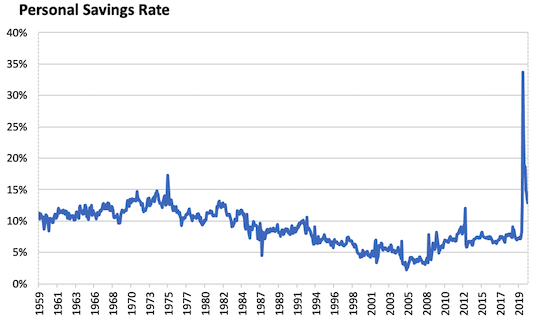

And personal savings:

Lots going on here. Let’s take it one at a time.

INCOME

Last year was the best year for income in American history. By far. It’s not even close.

A lot of the surge came from stimulus payments and unemployment benefits. But private wages and salaries are back at a new high. So are average hourly earnings. And weekly earnings.

These are not small numbers: Americans made $1 trillion more from March to November of 2020 than they did from March to November of 2019.

The stimulus part of the income equation is the most interesting to me, because it’s so big and has stuck around longer than most imagined.

It’s easy to write off a stimulus payment that boosts income as a one-time lift, not a new level of income that will be sustained or repeated. But that misses how much people love money. And once a new kind of stimulus money is tasted it becomes a permanent feature of how every subsequent downturn is handled.

A lot of the stimulus measures that took place in 2008 and 2020 – from industry bailouts to tax cuts to $1,200 checks – were things most people didn’t think were even possible before they happened. You might give your senator a pass for doing nothing if you think nothing is possible.

But now people know these things are possible, so they have a new set of expectations. No politician can look at unemployed Americans and say, “There’s nothing we can do.” They can only say, “We’re choosing not to do it.” Which few politicians – on either side – want to say when people are losing jobs.

So they stopped saying it.

In 1930, Treasury Secretary Andrew Mellon said, “Liquidate labor, liquidate stocks, liquidate real estate. Purge the rottenness out of the system.”

In 2020, Treasury Secretary Steve Mnuchin said, “We have a lot of money. We need to get that money in Americans’ hands.”

It’s a different world, and you ignore how much has changed at your own expense.

The $1 trillion stimulus package passed last week was a one-day news story, because it’s a fraction of the size of the CARES Act of last spring. A trillion bucks, big deal; that seems like the new view. But $1 trillion is more, even adjusted for inflation, than the 2009 stimulus package that made people’s jaws hit the floor and helped spark the Tea Party movement. Barack Obama writes in his recent memoir that when he wanted to do a $1 trillion stimulus his own chief of staff responded, “there’s no f**cking way.” It just seemed impossible. Now we do that and people yawn, and the biggest part of the story is that it’s only $1 trillion when it could have been $3 trillion.

Benjamin Roth noticed the same thing in 1934. He wrote:

People are no longer worried about government spending. An additional billion or two seems to mean nothing. When Coolidge was President in prosperous times he refused to pay the soldiers’ bonus for fear of inflation and the people agreed with him. Today, in the face of unprecedented deficits, the people see Congress approving the bonus and there is hardly a murmur.

Same story, same dynamic, just bigger numbers today.

The outcome in Roth’s day was the birth of Social Security. I wonder if our generation’s response to calamity is an enduring expectation of a thousand-dollar check per household whenever the economy dips. In any case, the numbers are enormous: Adjusted for inflation, the two stimulus packages passed in the last nine months are roughly equal to what we spent fighting World War II over four years.

It doesn’t matter whether you think stimulus packages and Fed policy are right or wrong or dangerous or immoral – that’s a different topic. What matters is that trillions of dollars have already flowed into households’ bank accounts in ways I don’t think people have come to terms with, because the numbers are so big they’re hard to contextualize.

It helps create a world where tens of millions of jobs are lost, but incomes surge to a new record. It’s a lot of cognitive dissonance to swallow.

DEBT

What do you do when you get a giant stimulus check and you can’t use it to travel because everything’s locked down, or go shopping because the malls are closed, or eat out because the restaurants aren’t open?

Millions of Americans used it to pay off debt.

Credit card balances declined by more than $100 billion over the last year. Americans have less credit card debt today than they did in 2007, despite an economy that’s 48% larger and has 30 million more people. There is no precedent for balances falling more than 10% in one year. But it just happened.

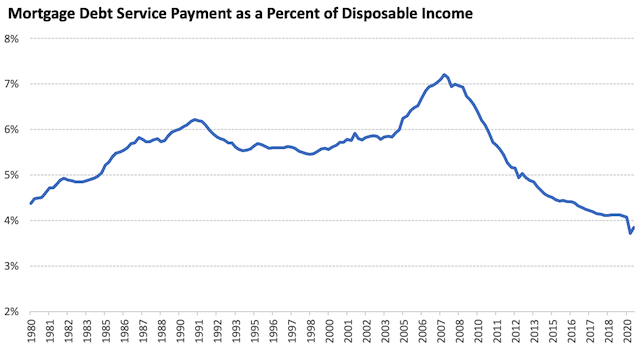

Mortgage refinancings also more than doubled in 2020, locking in interest rates that would have seemed like a joke a few years ago. Some companies are advertising 30-year fixed-rate mortgages for less than 2.3%, which can finance a half-million-dollar home for about $1,700 a month. Put differently: A $500,000 mortgage now has the same monthly payment that a $300,000 mortgage would have with 2007’s interest rates, and what a $210,000 mortgage had at mid-1990s interest rates.

The savings this has generated is astounding. In aggregate, mortgage payments as a percent of household income have declined from 7% of income in 2007 to less than 4% today, now a new generational low:

All of this happened while the homeownership rate has surged to the highest level since the housing bubble of the mid-2000s.

It also happened while nationwide home prices have grown an average of 6% per year over the last decade, eclipsing their previous bubble highs by a third.

Rising home prices have priced young buyers out because they require a growing and often insurmountable downpayment. But if you have that down payment, monthly mortgage payments as a share of income have never been lower in modern times. It’s a quirk that makes opposing narratives about home affordability equally true.

Student debt is still rising, though at the slowest rate in over a decade. Same with auto loans.

Add it all up, and total monthly debt payments as a share of income are now the lowest they’ve been on record, going back more than 40 years. In the last decade they’ve dropped from more than 13% of income to less than 9%.

For a household earning $50,000 a year, that’s a $2,000 annual increase in disposable income – about equal to the stimulus checks of 2020.

SAVINGS

Your spending is someone else’s income.

When you don’t spend, someone else gets laid off, which means they don’t spend, and someone else gets laid off, on and on.

Same thing works in the other direction. That’s why booms and busts have momentum.

And it’s why last March was such a red-alert moment for the global economy. Once spending stops due to lockdowns – and “stop” is hardly an exaggeration here – incomes collapse, and a nasty cycle takes hold.

Stimulus checks blunted the worst. Big portions of the economy figuring out how to operate with everyone working from home helped too.

But a lot of the spending still stopped. Vacations that would have been taken never happened. Weddings that would have taken place were postponed. Trips to the mall were replaced with aimlessly scrolling Twitter.

When income is replaced with stimulus checks but spending doesn’t rebound, savings surges.

Which is what happened in 2020, in an epic way.

The personal savings rate averaged 7% in the quarter-century before 2020. Then Covid hit, and overnight it went to 34%. It’s since dropped to about 14%, which would have been a 50-year high before Covid.

The result is that the amount of cash households have in the bank has absolutely exploded. I don’t even know if that word does justice. American households have $1 trillion more in checking accounts today than they did a year ago. For perspective, they held $800 billion in checking accounts a year ago. So it’s more than doubled. In one year. Benjamin Roth observed that “no one had any money” during the Great Depression. We now have so much I’ve run out of adjectives.

You begin to wonder what happens to that money once there’s widespread vaccination and the vacations, weddings, and mall trips that have been delayed are suddenly unshackled.

The best comparison might be the late 1940s and 1950s.

Then, as now, bank accounts were stuffed full as war-time spending brought record-low unemployment. And then, as now, a lot of that money couldn’t be spent because of war-time rationing.

After the war ended and life got on, the amount of pent-up demand for household goods mixed with the prosperity of war-time employment and savings was simply extraordinary. It’s what created the 1950s economic boom.

Fewer than two million homes were built from 1940 to 1945. Then seven million were built from 1945 to 1950. Commercial car production was virtually nonexistent from 1942 to 1945 as assembly lines were converted to build tanks and planes. Then 21 million cars were sold from 1945 to 1950.

Historian Frederick Lewis Allan wrote:

During these postwar years the farmer bought a new tractor, a corn picker, an electric milking machine; in fact he and his neighbors, between them, assembled a formidable array of farm machinery for their joint use. The farmer’s wife got the shining white electric refrigerator she had always longed for and never during the Great Depression had been able to afford, and an upto-date washing machine, and a deep-freeze unit. The suburban family installed a dishwashing machine and invested in a power lawnmower. The city family became customers of a laundromat and acquired a television set for the living room. The husband’s office was air-conditioned. And so on endlessly.

Could this be our future?

It’s tantalizing.

But I promised to avoid forecasts, focusing instead on what’s actually happened. And what’s happened – already happened – is that in many ways the American consumer is in the best financial shape in modern history, with minimal debt burdens and eager to spend their record savings.

The question is: why does that sound so absurd to so many people?

And I think the answer is fairly easy.

2. THE NEW SKEPTICISM

Microsoft CEO Satya Nadella says Covid pushed “two years of digital transformation into two months.”

The idea that Covid took a bunch of existing trends and sped them up is popular. We’ve seen it in everything from ecommerce to working from home.

We’ve also seen it in economic inequality.

Rising income inequality has been one of the most important stories of the last four decades. Then Covid hit, and the trend was fed rocket fuel.

Disclaimer: whether you think inequality is wonderful or terrible or what we should do about it is another story. I’m just focusing on what’s happened.

The causes of rising inequality over the last 40 years are vague. It’s part offshoring, part the decline of unions, part winner-take-all technology, part globalization, part regulation and tax code, part education, on and on. Complexity and vagueness made the trends subtle and slow.

Now the trends are suddenly stark and extreme.

A business can either operate in a pandemic or it can’t.

You’re essential or you’re not.

You can work from home or you can’t.

You’re open or you’re closed.

There are flight attendants and waiters whose careers vanished overnight, and lawyers/bankers/consultants/programers who continue earning their nice salaries and benefits from their couch. Dry Cleaners whose revenue fell 90%, and tech companies whose sales quintupled overnight.

In aggregate, the combination of stimulus and the majority of businesses figuring out how to operate in a pandemic has more than offset the losses. That’s why consumers – in aggregate – are in the best shape they’ve ever been in.

But the distribution of that prosperity has never been more extreme.

Take two recent CNBC headlines:

U.S. savings rate hits record 33% as coronavirus causes Americans to stockpile cash

61% of Americans will run out of emergency savings by the end of the year

Or these two:

Household wealth surged to a record high during the pandemic

More Americans are shoplifting food as aid runs out during the pandemic

That’s the story.

There are nine million fewer jobs today than a year ago, a decline of around 6%. But for those earning more than $28 per hour, the job market has fully recovered, like the recession never happened. For those earning less than $16 per hour, one-quarter of the jobs are still gone, which is on par with the 1930s.

This gets exacerbated by the way one person’s spending ends up as another person’s income.

Spending among the highest quartile of Americans is down 5% year over year, while spending among the bottom quartile is up 2.5%.

That might seem like the opposite of what you’d expect, but it perfectly explains what’s going on.

Low-wage jobs tend to be service jobs, which skew towards providing services for upper-income Americans – particularly in leisure and hospitality. To generalize, the spending-and-employment trend has gone like this: Wealthy people didn’t go on vacations in 2020. So their spending fell, and their savings went up. And the employees who would have served them on that vacation lost their jobs, only kept above water by enhanced unemployment benefits.

There are so many other skews.

As schools closed and at-home learning became a necessity, the norms of parenting broke down. A million people dropped out of the labor force in August and September, a stunning 800,000 of whom were women. The New York Times wrote:

… with many schools and child care centers still shuttered heading into the fall, many women — particularly white women — made the decision to bow out of the work force.

This sets up two distinct groups: can you help your kids learn from home, or not?

Another part of this that doesn’t get enough attention is how much technology has opened a window into how other people live.

To understand why so many people are so angry you have to realize that half the country gained insight into the other half at the very moment those halves were as different economically as they’ve ever been.

Think about this:

-

People gauge their wellbeing relative to those around them.

-

Historically, the people around you were relatively similar to you. They lived in the same city, went to the same schools, worked at the same factories, and earned similar wages.

-

The internet and social media increased the number of people “around you” exponentially.

-

It happened at the same time the economic distance between people ballooned.

Inequality has existed forever. Huge inequality, too. But people weren’t nearly as exposed to other peoples’ lives as they are in the digital era.

When the book How The Other Half Lives came out in the late 1800s – a book depicting squalor and poverty of tenement living – the New York Times wrote: “One-half the world never knows how the other half lives.”

Is that still true today? Sure. But much less than it’s ever been. Everyone is so much more interconnected, and the connections have no geographic boundaries. Before 10 years ago, everyone innocently lived in a relative little bubble.

In 1960 journalist Hugh Sidey attempted to gauge JFK’s economic credentials. “What do you remember about the Great Depression?” Sidey asked. Kennedy responded candidly:

I have no first-hand knowledge of the depression. My family had one of the great fortunes of the world and it was worth more than ever then. We had bigger houses, more servants, we traveled more. About the only thing that I saw directly was when my father hired some extra gardeners just to give them a job so they could eat. I really did not learn about the depression until I read about it at Harvard.

Again, could this happen today? Of course. But it’s way less likely in a world when people spend hours a day scrolling social media, looking at pictures and reading the casual opinions of other people.

It’s important, because when you’re exposed to people who are experiencing a different world than you are it becomes easy to ask, “Why don’t I have what they have?” on one end and, “Why don’t they have what I have?” on the other. Or just, “Why are you not like me?”

People have always asked that question. But the range of answers isn’t wide if the pool of people you judge yourself against is constrained to the town you live in or the company you work for. Once it’s expanded to 2.6 billion people commenting on Facebook posts, or a curated feed of Instagram vacation photos from Dubai and the Maldives, you enter a different world.

Benedict Evans nailed this years ago when he said, “The more the Internet exposes people to new points of view, the angrier people get that different views exist.”

And what have we done for the last 10 months? Covid has created vastly different points of view, and it’s given people lots of time to sit on the internet.

A hard thing to wrap your head around in economics is the idea that two opposite things can be true at once.

Consumers are in the best shape they’ve been in, ever.

A huge portion of consumers think that’s bogus because they’re in the worst shape they’ve been in, ever.

Both are true.

Two different worlds.